| With the first half of 2023 over it looks like the bear market for stocks is over. In fact, as previously discussed, the belief that the equity markets bottomed in June 2022 and then subsequently re-tested these lows at the end of September was in fact the bottoming process. That said, Investors went into the second quarter on high alert for a recession and thinking that North American Central Banks would be cutting rates by the end of the year. At the quarter’s end, there was still no economic downturn in sight, inflation remained sticky, and both the Bank of Canada and the FOMC in the U.S. were talking about further rate increases and keeping rates higher for longer. And thus, the three big questions remain top of mind for investors: - will interest rates continue to go up,

- will inflation make a return in the second half of 2023

- will earnings growth be sustainable for companies.

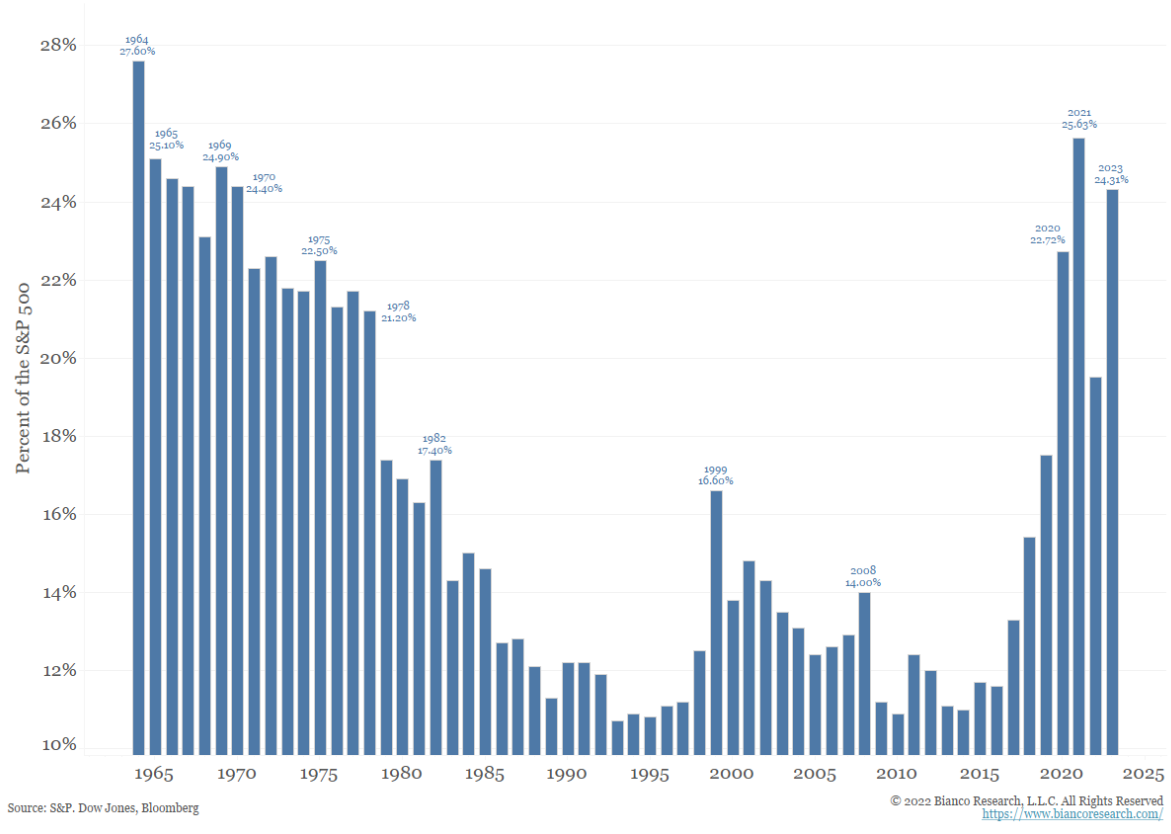

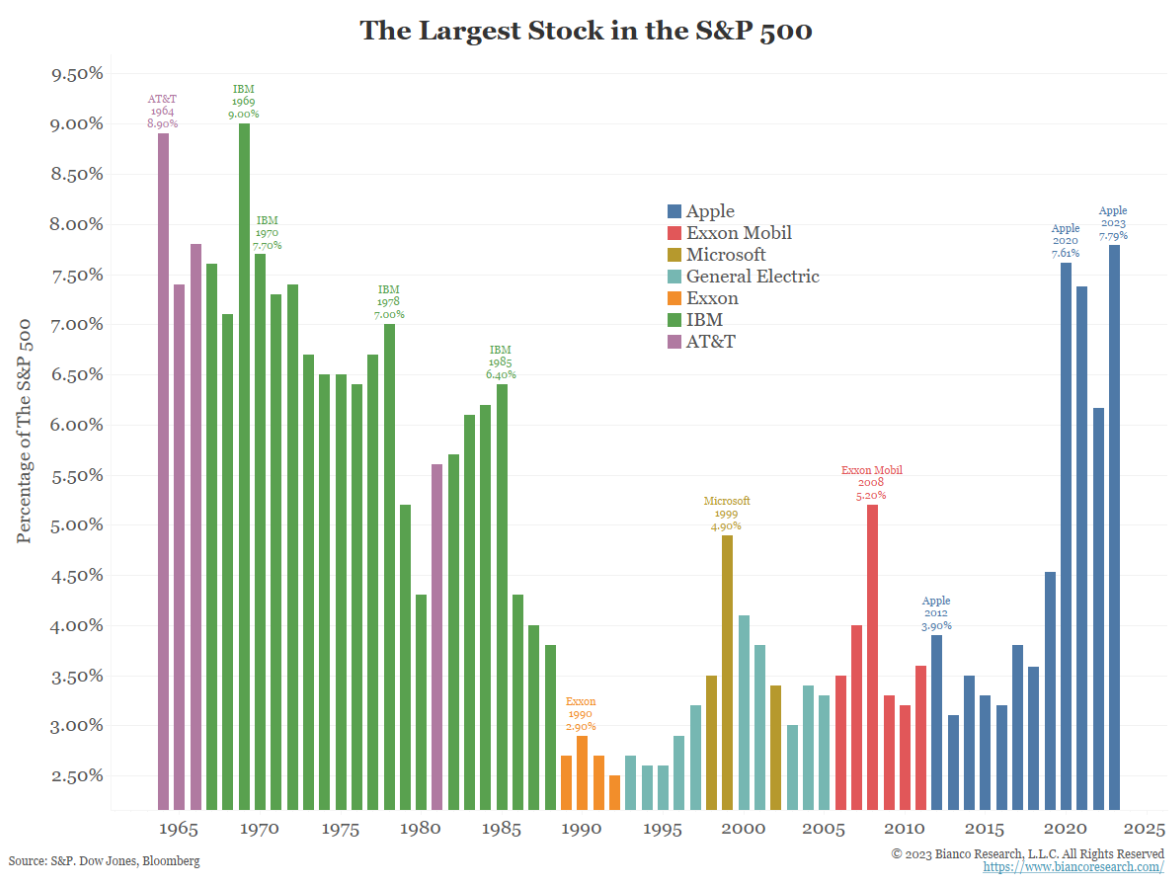

While all three of these questions remain unanswered at this point, our current positive outlook lies in the fact that markets have priced many of these uncertainties in and in fact 2022 was the year that valuations were corrected for these uncertainties. As markets get some more comfort that inflation is decelerating, interest rates have stopped their upward trajectory and earnings are not as bad as expected, there will be a re-rating of equity multiples which will lead to higher prices. The later has already started. In Canada, despite the Energy, Material and Financial sectors being weak, the TSX has managed to return 5.76% for the quarter. Keep in mind that these 3 sectors make up 62.5% of the index so the rally has been broad year-to-date. In the U.S., investors have the opposite problem. Despite even stronger returns of 14.28% for the S&P 500 for the quarter, the rally has been very narrow with the 8 largest stocks in the S&P 500 driving most of the return. These eight large stocks now make up 25% of the S&P 500 index, so as these companies go, so does the index. Looking at the index on an equal weighted basis, returns are much more level. Looks like passive investing will win this quarter as it would be hard pressed to find any US Equity manager with 25% of their portfolio in a few names.

The leading contributors were tech giants Apple APPL (up 17.8% for the quarter and 49.6% for the first half of the year), Microsoft MSFT (up 18.4% for the quarter and 42.6% for the first half), Nvidia NVDA (up 52.3% for the quarter and a whopping 189.5% for the first half), and Amazon AMZN (up 26.2% for the quarter and 55.2% for the first half). 2023 has seen the best first-half performance for the Morningstar US Technology, Communication Services, and Consumer Cyclical Indexes in their entire tracked histories (since 1999). The Fed Pauses (or ‘Skips’) Rate Hikes and BOC Resumes Hikes. The BoC had seen enough by early June to go back on its ‘conditional pause’. An inflation setback, resurgent housing markets and resilient jobs/GDP growth collectively implied that monetary policy was not restrictive enough. There’s an air of data- dependency here, which adds some near-term uncertainty, but having resumed hiking in June, the path of least resistance has been to discount additional tightening this quarter with one additional hike to 5% in the coming quarter (which just happened on July 12). In its continued effort to reign in decades-high inflation without engineering a recession, the Federal Reserve raised its benchmark effective federal-funds rate an additional 25 percentage points in May, then held rates steady for the first time since January 2022 at its June meeting. US government bond yields had a turbulent end to the quarter as U.S. data releases gave conflicting signals over the strength of the labor market. Markets (along with many economists/strategists) continue to come to terms with the ‘higher for longer’ narrative in fixed income markets. Recent releases have underlined our view that the Federal Reserve faces a tricky balancing act in achieving a soft landing as: • Labor market strength still looks inconsistent with the Fed’s inflation target • Core measures of inflation have been falling, but slower than expected. • The services sector still looks strong, while the manufacturing sector has been contracting for the past eight months. For policymakers, it’s about appearing resolute in the face of still- elevated inflation. One presumes it will take more relief to soothe inflation-frayed nerves at many of the world’s central banks. To us, the economic cycle—including material weakness across key parts of the global economy—should secure the long-awaited inflation relief that central bankers so desire. We see a growing collection of indicators pointing to moderation ahead—for American growth, jobs, and business investment—which could see the FOMC setting the table for less restrictive policy in the new year. Bottom line: Our overarching theme is that capital markets. Investment results are better than expected because the economic situation is largely better than expected. Equity market returns across the globe are generally positive. Many pundits have been predicting a recession since the middle of 2022 (à la waiting for Godot). These downbeat expectations saw 2023 open with bonds and stocks positioned for upside should good surprises arrive. So far they have as corporate earnings, employment, and GDP growth have generally come in better than anticipated. Some equity markets are close to reaching our full-year forecasts. We called for equity returns in the neighborhood of 8% to 12%, seeing targets of 22,000 for the S&P/TSX Composite and 4,400 for the S&P 500. We are comfortable with our TSX target and plenty of upside room for the TSX to hit 22,000. While it’s still early, we are penciling in 5,000 as reasonable for the S&P 500 next year; there may well be progress toward this level in the back half of 2023. The most important factor in our analysis is earnings growth, which is improving against an improving economic backdrop. This progress underpins our continued enthusiasm for equities. Our portfolios remain well balanced, with a modest tilt toward equities. After harvesting some gains earlier in the year, the continued outperformance of U.S. stocks is nudging our exposure up. We are watching this situation closely but allowing the drift to persist so that our equity overweight has grown a little (from slight to modest). We are now overweight both Canadian and U.S. equities in many portfolios. As we trimmed galloping positions in U.S. equities throughout the year's first half, we closed our underweight in international developed markets (Europe and Japan). Additionally, in portfolios with exposure, we rotated some Canadian and U.S. large-cap equity exposure into small- and mid-caps. Our well-diversified exposure to bonds is delivering a solid running yield. Coupon income and maturity proceeds are being reinvested at higher yields. While this is not our base-case scenario, if the economy slows too much we believe our bond positions will provide a level of safety. |