Don't Go Chasing Waterfalls

Andrew Hill - Jan 11, 2022

Please stick to the simple, diversified portfolios you’re used to.

The underlying message of the popular early 90s R&B hit was to avoid self destructive behaviour in the pursuit of ambitious goals.

Ambition isn’t a bad thing. It can be a very good thing. It can be the fuel for our grand pursuits. But it can also blind you to the realities around you.

In the investing world, the waterfalls are the hot trends, hot stocks or hot funds.

Investors are forever seeking get rich quick opportunities, and the illusive free lunch (ie. exceptional returns with minimal risk)

This ambition has manifested itself repeatedly: Japan in the 80s, tech in the 90s, the FAANG stocks in the late 2010s, and crypto/NFTs today.

The problem isn’t that these are poor investments (FAANG stocks are generally still going strong). The problem is that, from time to time, the hype drives the price of these investments far beyond reasonable expectations. There is old investment saying, “the difference between a good company and a good investment is the price that you pay for it”

It can be very difficult for the average investor to separate the signal from the noise (ie. the meaningful information from the interference).

Here are a few things to be considerate of as you separate what is important from what is not:

1. The markets make the news, the news does not make the markets

10am: “Markets up on consumer sentiment”

2pm: “Markets down on consumer sentiment”

As investors we are forever looking for a sense of control and understanding in places that it sometimes does not exist. The same is the case for the financial media.

Don’t concern yourself too much with the headlines. They will flow as the markets flow. The more gratuitous the headline, the less instructive it is for investing.

2. The greater the concentration, the wilder the swings, the harder it is to stick to the plan

I have said it before. Concentrating your wealth in a small number of holdings is a great way to multiply your assets, but also a great way to lose them all.

The added challenge is that individual stocks are generally significantly more volatile than a diversified basket of stocks. Amazon has been one of the best investments of the past few decades. It has averaged 38% per year since it’s IPO. But it has also experience many 10-20% drops over very short periods of time (ie. a few days). In the dot com bubble, it lost 90% of it’s value. Appreciating an investment with hindsight is easy. Living through the volatility is hard.

I am not averse to owning a small number of individual names, particularly for those who can afford the losses. But you should have a very strong understanding of the business, a high degree of conviction in its growth story, and a clear understanding of what the cost may be if you are wrong.

3. The bigger the returns, the harder they are to repeat

Cathie Wood (of ARK Investment Management) and famed SPAC pioneer Chamath Palihapitiya rose in prominence throughout 2020 for their mind-blowing returns. The financial media crowned them, and investor money came quick. Yet in 2021 they came crashing back down to earth.

Their story is not atypical. A thematic trend takes hold (tech growth stocks in this case), a select number of managers significantly outperform, they garner media attention, investors pour in, and they subsequently miss expectations. This doesn’t mean they are bad managers. It is simply because it is very difficult to consistently be a rockstar. Even the fund managers with the best long-term track records experience at least 3 years of underperformance every 10-year period.

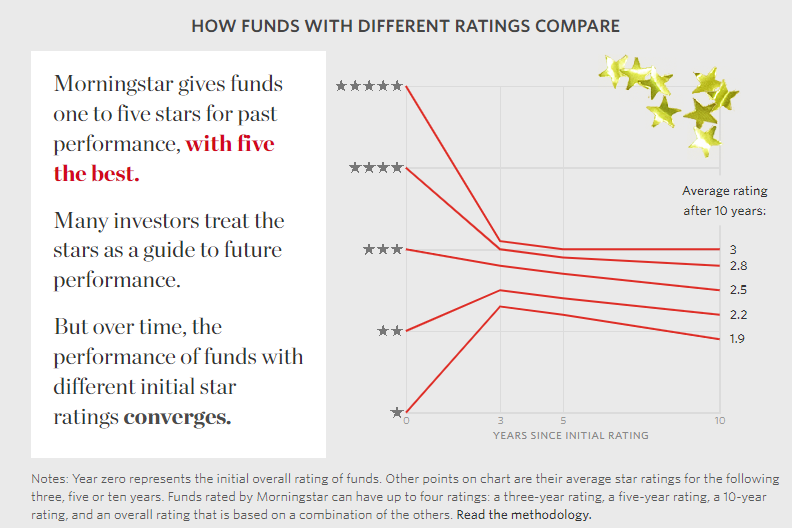

This became crystal clear in 2017 when the Wall Street Journal looked closely at Morningstar’s star ranking system.

Morningstar is a company who would take thousands of mutual funds and ETFs and distill their performance into an understandable ranking system. Their stars were a blend of 1, 3, 5- and 10-year returns. So, naturally, the better the performance the higher the star ranking.

And, as expected, the higher the star ranking the greater the inflows from investors.

In 2017, the Wall Street Journal looked closer at the star system from 2004-2014. What they found was that it was more likely for 5-star funds to see a performance decline and for 1-star funds to see a performance improvement (ie. you were better off investing in the worst ranked funds)

Source: wallstreetjournal.com

In a world of immediate, overwhelming information, it can be difficult to separate the signal from the noise.

As an investor you need to understand that very few themes persist for long periods of time. Trends come and go. While it can be lucrative to ride them up, it can be painful to ride them down.

You need to remain disciplined and systematic with a specific goal in mind.

As always, it’s best to just keep it simple