7 Things I Think I Think About The Market

Andrew Hill - Nov 01, 2021

1. The Stock market is not exactly the economy

Being concerned about the economy is one of the most common reasons why people are reluctant to invest. This shouldn’t come as a surprise. People are generally predisposed to be more guarded and pessimistic rather than open and optimistic; especially with their wealth.

But the fact of the matter is that the market is not the economy. The market will generally take its cues from the economy, and trend in the same direction. You can’t have a thriving market without at least the expectation of robust economic output. But the two don’t move in tandem.

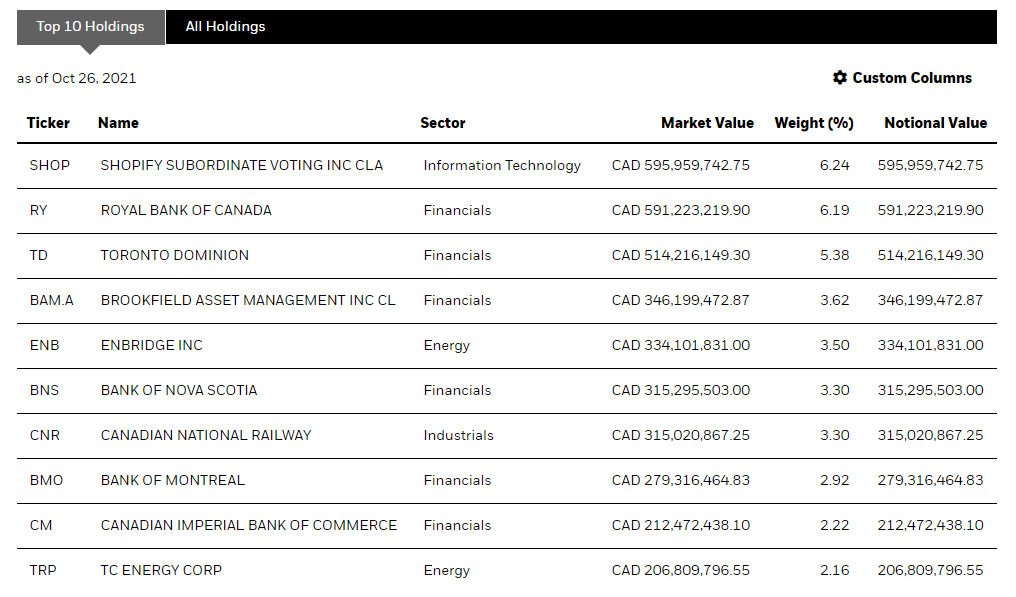

For example, the weights of the top 10 holdings of the S&P TSX Composite Index represent 38.83% of its total. The top 5 banks alone contribute 20%. Yet, no one would argue that these companies’ contribution to GDP would match their market weight. Canadian Banks likely only contribute approximately 3.5% to GDP (source: Canadian Bankers Association)

Source: S&P Global

Moreover, markets are forward looking. The economic data of today only tells a part of the story of the market price.

Investing Lesson:

- Don’t take your investing cues from your feelings about the economy. Company earnings, cash flow, leverage, etc. are far more consequential to the growth of the stock market.

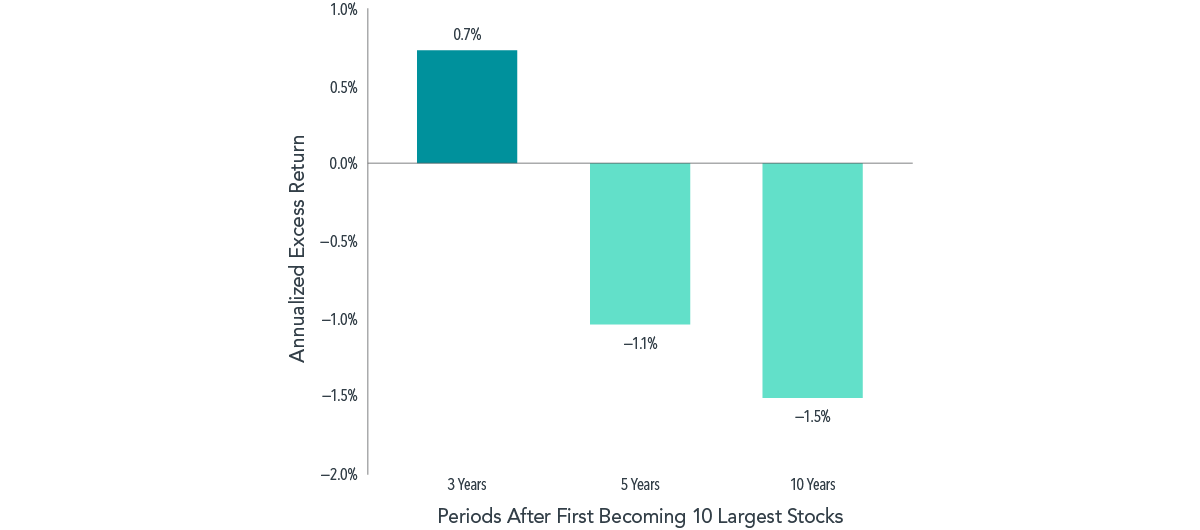

2. The big winners of the past 5 years will likely not be the same for the next 5 years

It is difficult to imagine an S&P 500 that isn't being led by today's big tech.

But that prospect is probably more likely than it is unlikely. Jeff Bezos himself predicted that Amazon would one day go bankrupt.

On average, the top 10% of S&P 500 companies in the past have gone on to underperform the market for the next 5 and 10 years. Valuations matter far more in the long term than they do in the short term

Annualized return in excess of market for stocks after joining list of 10 largest US stocks, 1927–2019

Source: Alpine Macro

Investing Lesson:

- It’s easy to get caught in a hot trend, but long term investment success depends on a diversified approach that separates the signal from the noise.

3. Market corrections aren’t a bug, they are a feature

Imagine your stomach had no way of telling your brain that it was full. While the short-term joy of consuming more (candy for me) would be a positive, the long-term implications to your body would be far worse. Your stomach has stretch receptors to tell your brain that it’s time to slow down or stop.

Market corrections serve a similar purpose. They level set prices to better reflect expected underlying earnings. They also level set us psychologically and balance our perspective.

Investing Lesson:

- Plan for a correction of at least 5-10% every year, but don’t worry too much. The longer your time horizon, the less they matter.

- The more corrections you live through, the easier they become.

4. Plan for an average, but don’t expect it to be average

Investment conversations and wealth plans are, understandably, set around an average expected rate of return of some sort.

This makes complete sense. Your typical investor wants to anchor their expectations in order to gauge their future success. And every wealth planner needs to set a benchmark to meet to ensure that a client’s investing goals are achieved. However, averages are decidedly not average.

Take the following two 5-year sequences of annual returns.

5%, 5%, 5%, 5%, 5%

-12%, 21%, -9.5%, 20%, 10.4%

Both result in the same geometric average, but the experience along the way is extremely different.

Investing Lesson:

- Markets are fickle. They digest information quickly and opinion can sway rather rapidly. Large downward swings are often followed closely by large upward swings. But that doesn’t mean that expectations should change. Stick to the plan and only adjust when you can be sure that expectations have changed.

5. True risk is the unknown unknown

As Donald Rumsfeld famously said, “There are known knowns. These are things we know that we know. There are known unknowns. That is to say, there are things that we know we don't know. But there are also unknown unknowns. There are things we don't know we don't know.”

Investing is ultimately an exercise in estimating the future. Stock analysts estimate future cash flows, Bond analysts estimate the path interest rates, Economists estimate inflation, output, productivity, etc.

While it is difficult to consistently be perfect, these sorts of things can be estimated within a reasonable range.

But true risk is the meaningful events that have a long lasting impact on the market, which you couldn't reasonably foresee.

For example:

- COVID-19 (downside risk)

- The historically unprecedented fiscal response to COVID-19 (upside risk)

- The fall of Lehman Brothers (downside risk)

- QE1, QE2, QE3 in response to the financial crisis (upside risk)

- The fall of the twin towers (downside risk)

Investing Lesson:

- Fight your overconfidence bias. Understand that there are things we can’t control or predict. Build your portfolio to plan for the worst, but expect the best.

6. Concentrating your assets is a great way to multiply money and a great way to lose it all

Charlie Munger (Warren Buffett’s long-term business partner) was famously quoted as saying that “using volatility as a measure of risk is nuts. The risk to us is 1) the risk of permanent loss of capital, or 2) the risk of inadequate return”.

Everyone has a friend or family member who made a truckload of money investing in something. Maybe they bought Apple 20 years ago or Bitcoin 5 years ago. It can be very difficult to ignore the siren song of a 10x return, instead of steady and stable long-term compounding growth.

But always remember that it’s far easier to openly brag about your winners rather than to be publicly humbled by your losers. For every Apple there are at least 10 Pets.com.

While the upside of concentrating your bets can be very lucrative, the downside can be catastrophic, as losses are often irreversible.

$1000 dollars invested in Bitcoin in November 2016 would be worth ~$76,000 today.

But $76,000 invested in Enron, Worldcom, Lehman Brothers, or pre-financial crisis GM is worth nothing today.

Investing Lesson:

- Don’t put all your eggs in one basket. If you want to speculate and take an outsized bet on one investment, don’t risk more than you are willing to lose

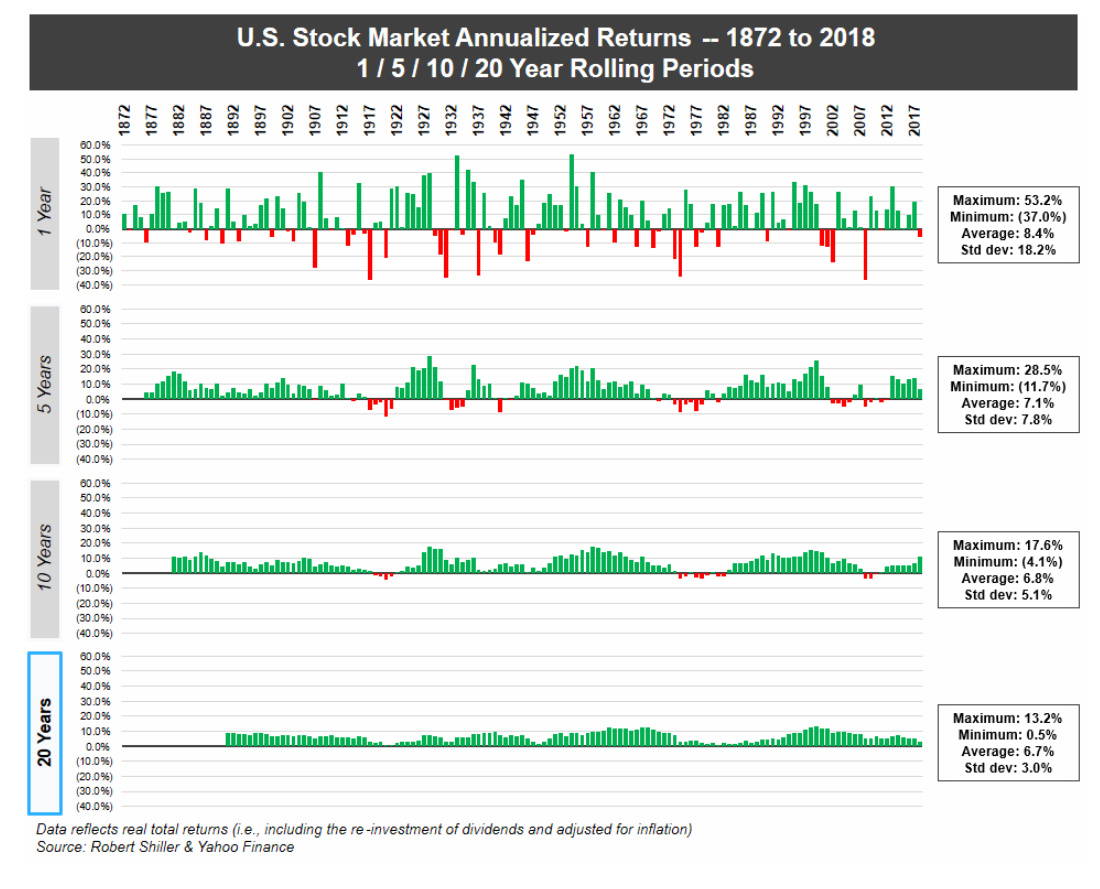

7. The Long Game Is The Only Game In Town

In the short term, the stock market can feel like a casino. On a day to day basis, it probably is. The odds of the market being up or down on a given day are pretty well the same as the roulette ball landing on black or red. In fact, it’s not a whole lot better on a month to month basis either.

But the longer you stay at the table, the more that your chances look like that of “the house” and not those of the gambler.

There is a reason why investment professionals will tell you that it's a long-term game. It’s because it is true. The longer your time horizon for investing, the greater the likelihood that you will come out comfortably on top.

Investing Lesson:

- For any funds you may need in the next 1-3 years, you probably shouldn’t invest in the stock market; unless you understand the risk that you may be drawing on it at a lower value.

- Compounding is the 8th wonder of the world. The longer you allow your wealth to grow, the larger it will become