A Rule of Thumb For Rules of Thumb

Andrew Hill - Jul 08, 2021

Always get 8 hours of sleep

Cook your chicken 20 minutes per pound.

Make sure your lawn gets an inch of water every week

Rules of thumb have likely been around for as long as humans have had to make quick and simple decisions. The phrase itself has been in circulation since the 1600s. The earliest known print was found in a sermon in 1658:

“many profest Christians are like to foolish builders, who build by guess, and by rule of thumb and not by square and rule”.

But it wasn’t until recently that behavioural psychologists tried to better understand why we use rules of thumb. In their seminal work “Thinking Fast and Slow”, Daniel Kahneman and Amos Tversky popularized heuristics. These are mental shortcuts – the internal, subconscious rules of thumb - that our brains take when we are required to decide quickly in the face of pressure. We will almost always default to “system 1” – the fast thinking subconscious part of our brain - rather than “system 2” which is the slow thinking, rational part. Thinking slow costs more calories than thinking fast.

Although this approach can be beneficial when deciding whether to flee from a lion, it can be hazardous to our long-term financial success.

Let’s look at some of the more common investment and wealth management rules of thumb, along with alternative, potentially better ways to approach them.

Sell in May and Go Away

Frankly, this one should be sold immediately, never to return.

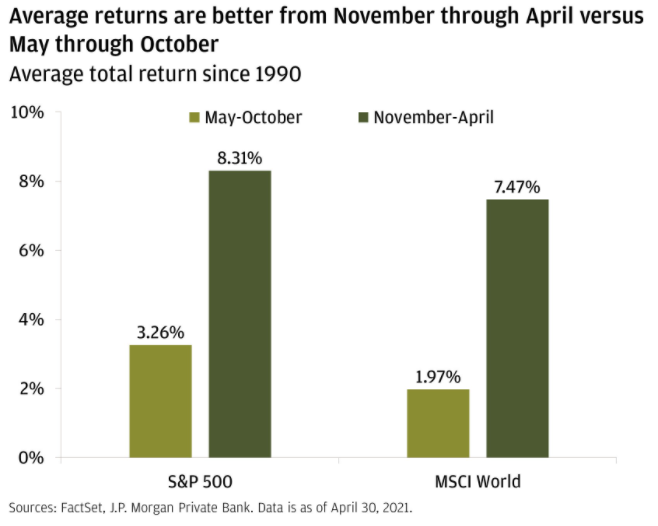

Every single May, without fail, this rule of thumb reappears. It asserts that you should move your portfolio to cash at the beginning of May and buy back at the end of October.

While it is true that the period from November through April tends to deliver stronger returns than from May through October, returns are still generally positive in both periods. Moving to cash would typically lead to missed opportunity.

What should you do instead?

- Sell if you need the cash.

- Sell if your investment thesis or plan has changed.

- Sell if you have a more attractive investment option.

- Above all, it’s generally best to simply remain invested.

Withdraw 4% of your portfolio every year in retirement

This rule of thumb suggests that your portfolio will last you well into your golden years, if you only withdraw 4% of the total value every year.

This one is well-intentioned and has proven to be reasonably effective. But there are far more efficient and accurate ways of assessing how much you can drawdown each year in retirement.

It’s the equivalent to that relative who insists on giving you directions to their house even though you have an iPhone. Both may get you to your destination, but one will do it much more accurately and efficiently.

The beauty of the 4% rule is in its simplicity, but so too is its downside. No two people are the same; lifestyles, income streams and appetite for risk all contribute to how much you can draw from a portfolio sustainably.

What should you do instead?

- Put together a financial plan. It’s the easiest and most accurate way to digest all your information and come up with a suitable plan. But much like your GPS re-routes you because of an accident, the same goes for your financial plan. It should be reviewed and potentially revised on a regular basis.

110 minus your age should be the amount of stock you hold in your portfolio

This rule says that to determine how much stock market exposure you should have, simply subtract your age from 110 (ex. a 50 year old should have 60% stock market exposure).

I’m not even sure that this can be classified as a rule of thumb because it has changed so much over the past 25 years. The rule used to be 80 minus your age, and then 90 minus your age, etc. This likely reflects steadily declining interest rates and returns on fixed income investments.

But, again, no two people are alike. An 80-year-old may have a stronger stomach for market drops than a 50-year-old. A 70-year-old may be drawing far less on their portfolio than a 60-year-old. An 85-year-old may have different legacy goals than a 65-year-old.

110 minus is far too simplistic.

What should you do instead?

- Build your investment plan around your financial plan.

- Determine how much you will likely need to withdraw in the next 3-5 years. This can be a reasonable floor for fixed income producing assets you should hold, if you can't meet your expense needs through income alone.

- Determine what kind of legacy you would like to leave and what kind of returns you need to get there.

- Try your best to figure out what kind of drop in your portfolio you can tolerate before you just can’t take it anymore (note: this is probably the hardest part as it changes over time). This will help to define how much equity vs fixed income exposure you should take.

- Accept that your answers to the prior 4 points may conflict with each other and make adjustments where necessary.

The 50/30/20 rule

50% of your income should go to necessities, 30% to discretionary spending, and 20% to savings.

This is a great rule if only because it encourages stable, predictable saving.

But (and I can’t stress this enough), no two people are the same!

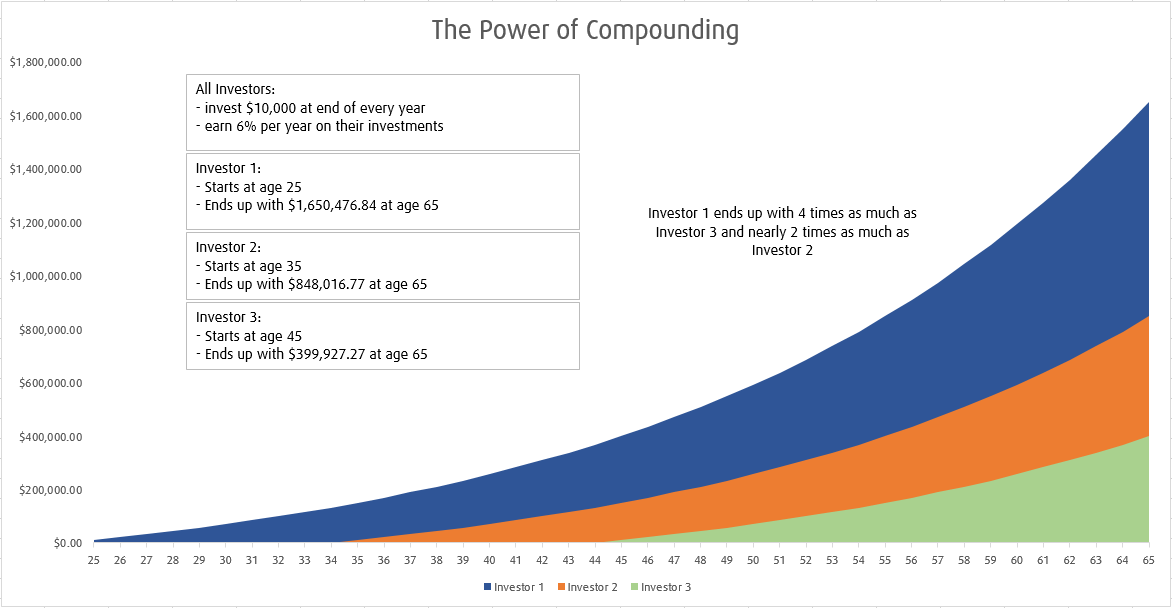

When you start saving is as important as how much you are saving

“Compound interest is the 8th wonder of the world. He who understands it, earns it…. He who doesn’t, pays it” – Albert Einstein

- Establish what you would realistically like to spend now and into retirement. And then, using reasonable rate of return and inflation expectations, determine how much you need to save to get there. The sooner you start, the easier it will be.

- If 2+2 = 3, then you will need to make some revisions. Often this means spending less now to spend more later; but it may also mean tweaking your investment strategy to try and meet your goals.

We are fortunate enough to live in an age where we don't need to spend many calories to come to more intricate, rational conclusions. The technology and professional expertise exists to provide the guidance necessary so we aren't stuck relying on inefficient, dated equations.

My only rule of thumb is not to use them at all.