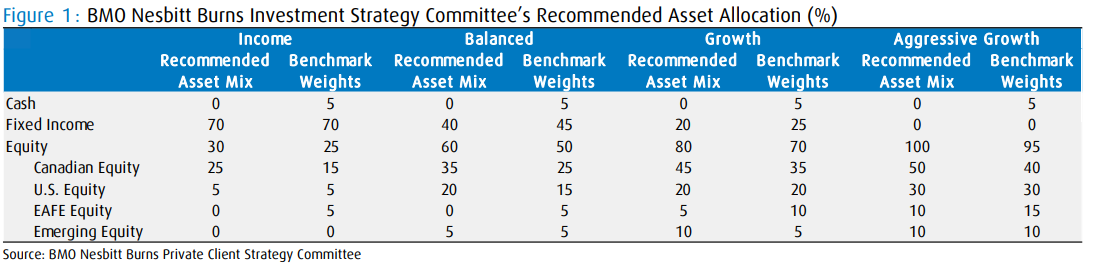

Investment Strategy

BMO Private Wealth - Sep 19, 2024

We don’t often think of Switzerland and Canada leading the developed world, but that is exactly what these two countries have recently done, at least in terms of central bank rate cuts.

Ladies and Gentlemen, Rev Your Engines

We don’t often think of Switzerland and Canada leading the developed world, but that is exactly what these two countries have recently done, at least in terms of central bank rate cuts. But coming fast on the outside is the U.S. of A. None other than Jerome Powell, Chairman of the Federal Reserve (“Fed”), confirmed last week that “the time has come” to lower rates at the upcoming September 17-18 meeting. This is fully in line with market expectations, with a 0.25% cut fully priced in for a while now. While the element of surprise will be absent, the fact that the world’s most important central bank will cut because of the continued positive inflation trend (a good reason) means that the impact should be positive for both bonds and equities (we present a historical discussion below, but the punchline is that Consumer stocks and Healthcare tend to be great performers). So, the year 2024 should continue to look like the mirror image of 2022 in our view. Many investors have painful portfolio memories from two years back as both fixed income and stock positions were down significantly, a rare occurrence indeed. The fault for this rested squarely on rampant inflation, which, as our readers know well, is poisonous for financial assets. Since then, however, both the Fed and Bank of Canada (“BoC”) have managed to bring price levels under control while potentially engineering a “soft landing”, a desirable outcome where the economy slows down without incurring a recession.

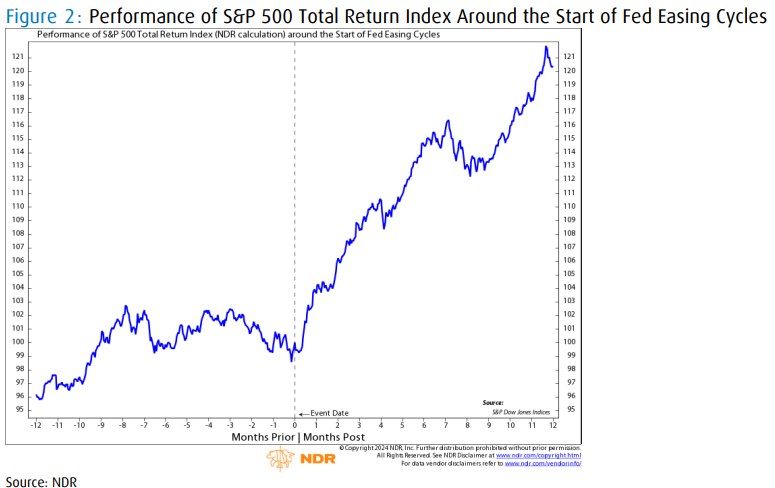

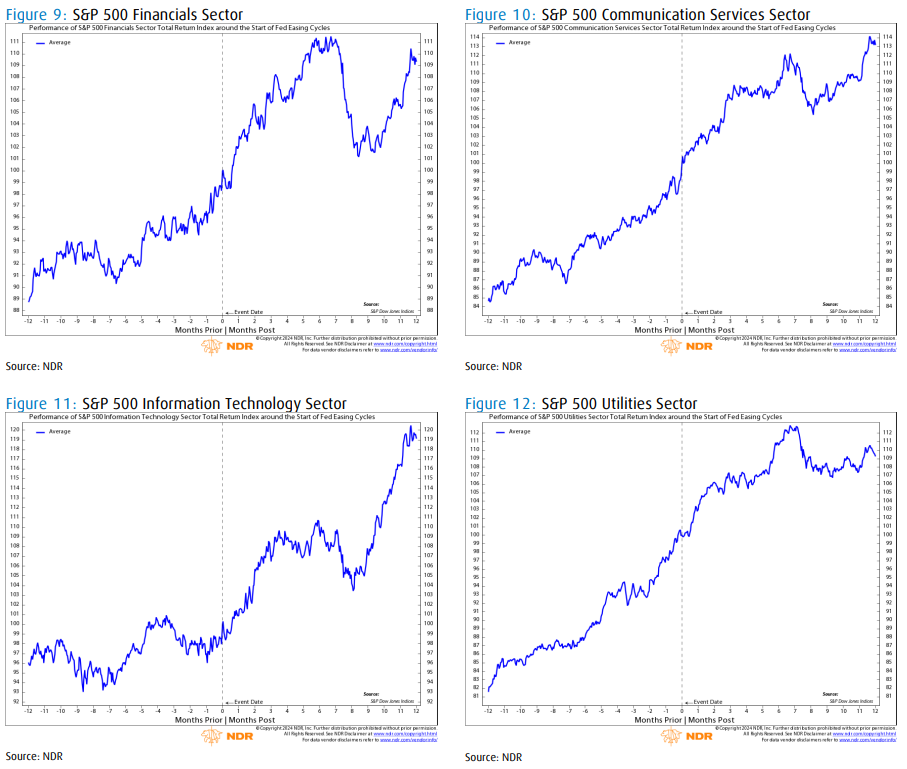

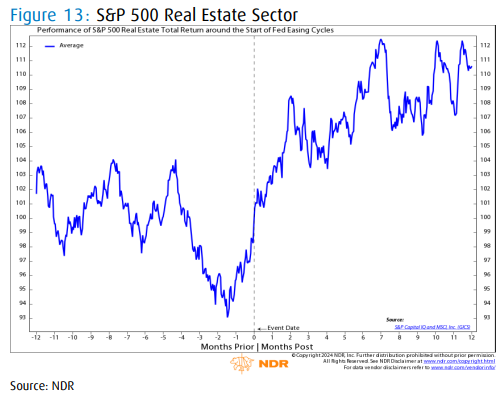

As we have noted before, stocks typically post strong gains during easing cycles. Based on data collected by our research partners at NDR, going back to 1928 (encompassing an impressive 22 Fed rate cut cycles), mean returns turned positive almost immediately following the first Fed rate cut, with 20% average annualized total returns 12 months after the first rate cut. This represents more than 10% better performance vs. the market’s historical return (i.e., including non-easing cycles). Of course, every cycle is different and contains idiosyncratic drivers. Still, the results make intuitive sense since a lower cost of funds helps consumers and corporations, and a lower “risk-free rate” increases the value of existing bonds and the present value of corporate free cash flows.

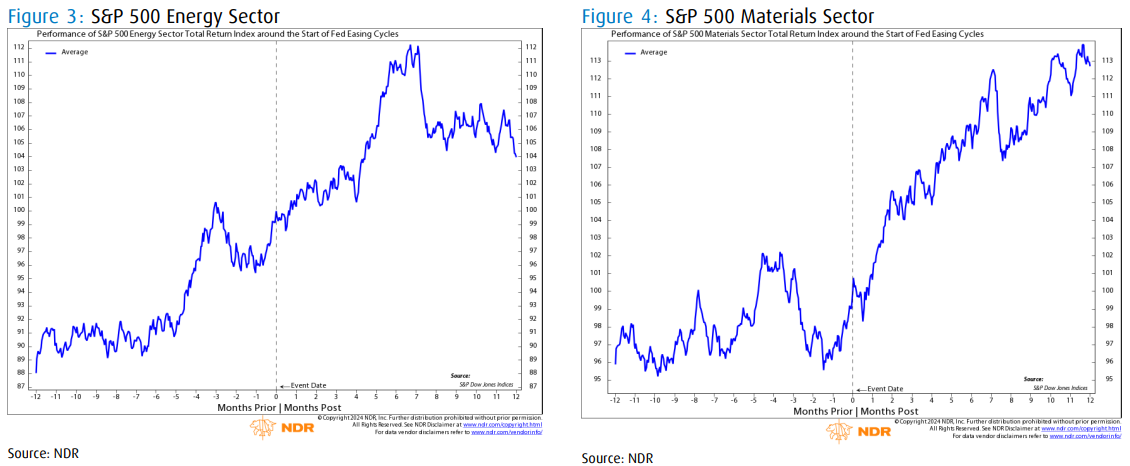

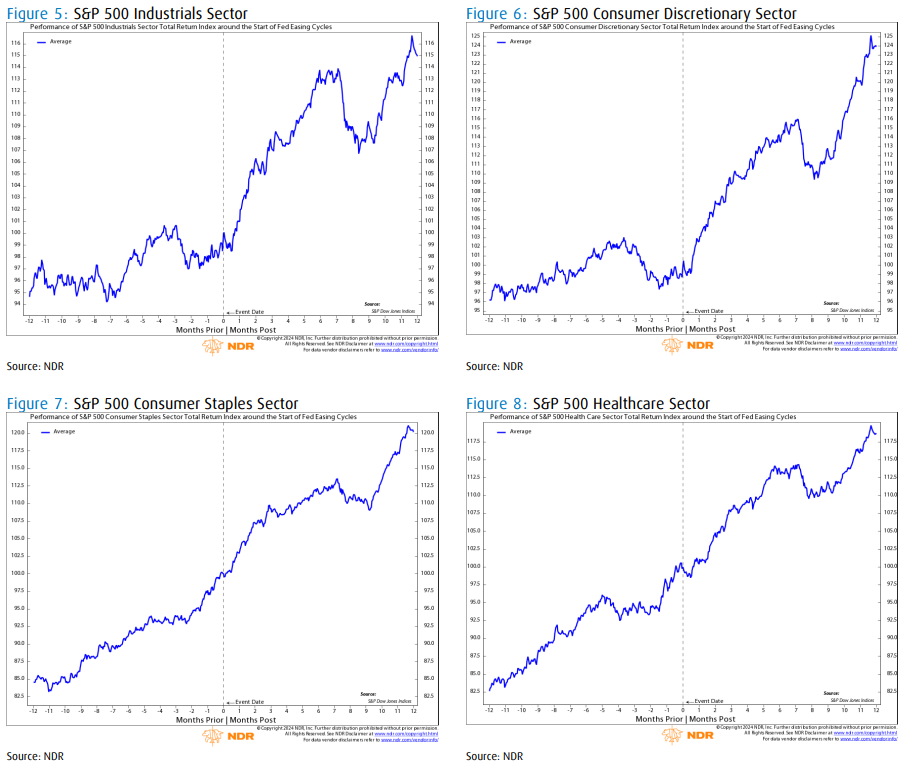

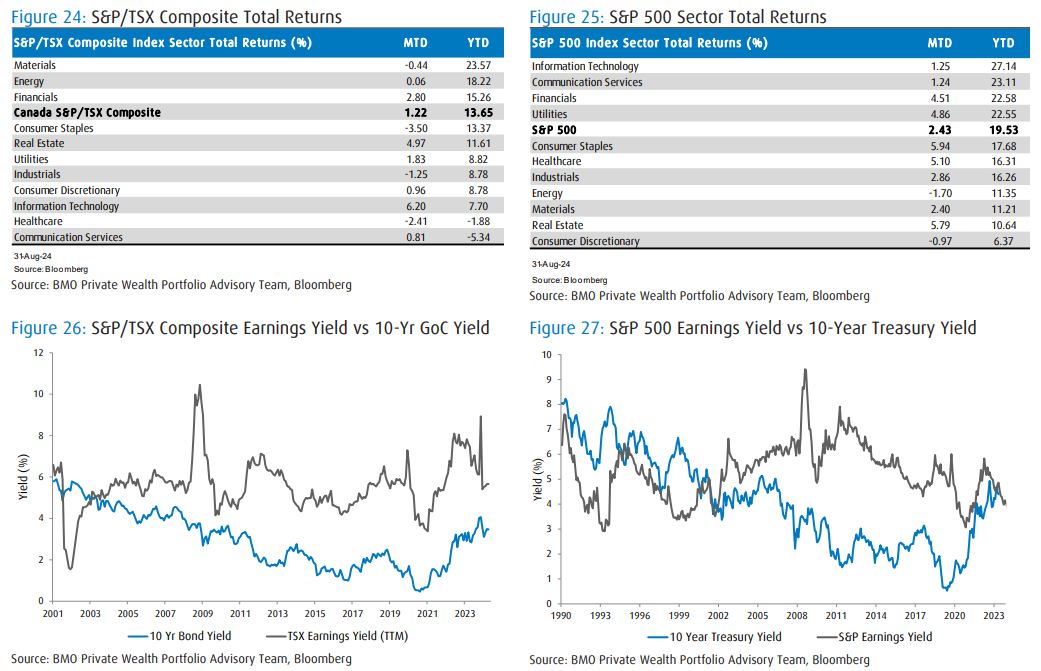

Digging down to historical sector performance yields similar positive results, with all 11 super sectors delivering high single to low double-digit returns six months after the first rate cut (note that this data begins in 1972, so it is not strictly comparable to the index data above). This is the “rising tide lifts all boats” period. Interestingly, after that point, performance does start to diverge meaningfully. Top performers include Consumer Discretionary (+24% total return), Consumer Staples (+20%), Tech (+19%), and Healthcare (+18%). Energy on the other hand has tended to give up some of its gains and returned a much more modest 4% on average. Having a good sense for the fundamental drivers of the current cycle and performance leading up to the first rate cut are also very important since no two cycles are identical as noted above. From that perspective, we suspect that front-ended market strength in the first half of 2024 will reduce the market’s total return vs. history, particularly for the Tech and Consumer Discretionary sectors. Conversely, the compelling value in Canadian Energy stocks could make that sector outperform its history.

Below are charts highlighting the total return performance of various sectors around the start of easing cycles.

Technical Analysis

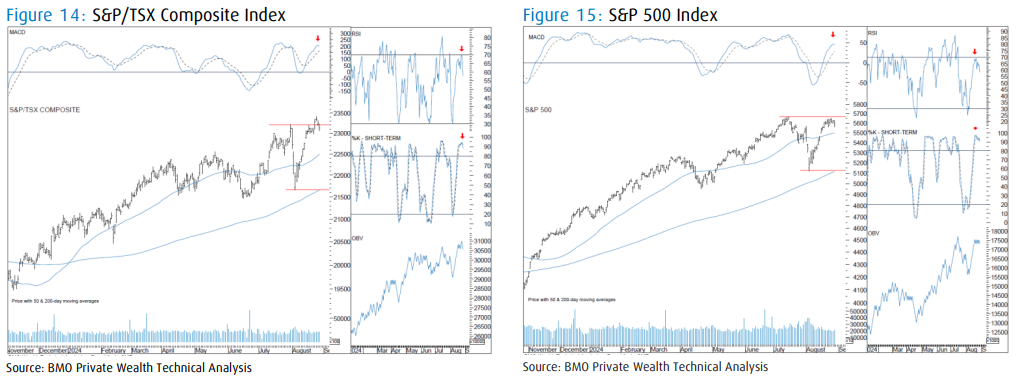

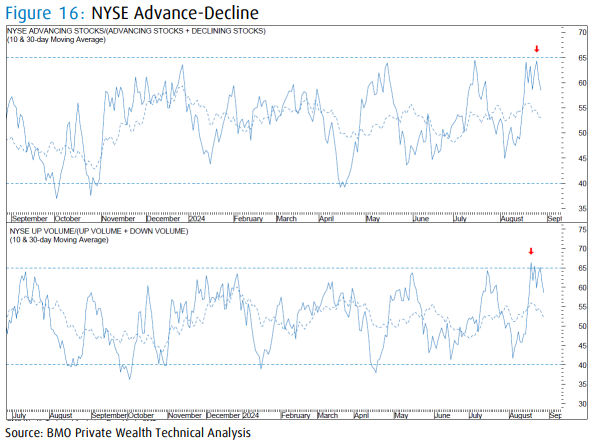

September is traditionally the weakest month of the year for stocks both here in Canada and the United States. Over the past few decades, the average return for the S&P/TSX Composite Index in September is -1.57%, and -0.66% for the S&P 500. This year it’s shaping up to be more of the same since all the indicators in our short-term timing model are in the midst of rolling over and going negative from at/near oversold extremes.

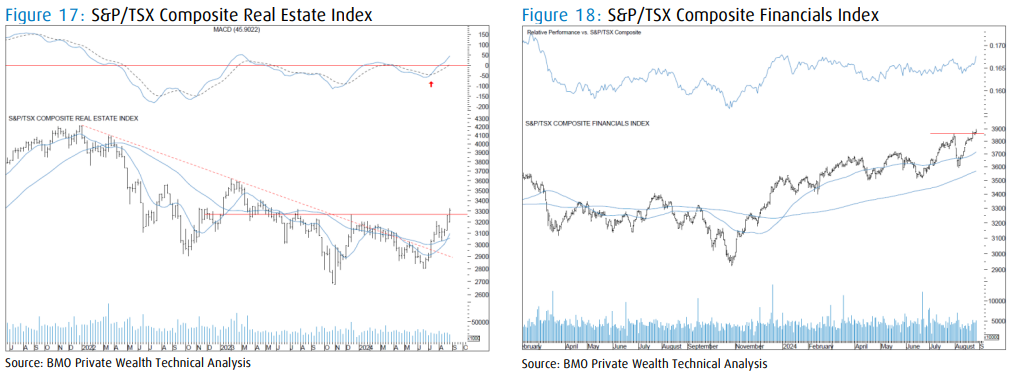

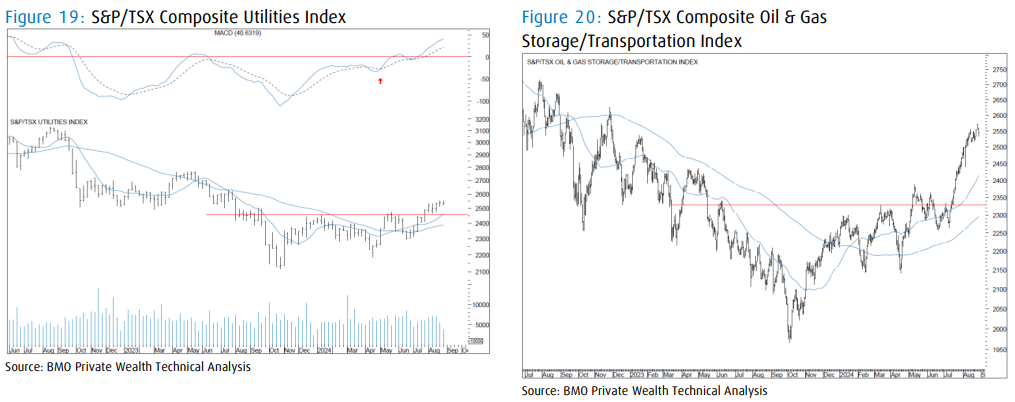

Because of this, we are likely to see a re-test of the early August lows to some degree as part of a larger medium-term corrective process that began in late July (TSX: 21,659, SPX: 5,119). The good news is that it will likely represent the final phase of the correction and should set the stage for further new highs into the fourth quarter and beyond. As such, any weakness that develops in September should be considered the best buying opportunity since last October’s medium-term correction low. In terms of where we would focus our buying, interest sensitive areas look the most compelling right now due to persistent weakness in long-term interest rates. REITs, Financials, Utilities, and Pipeline stocks have all recently broken out of multi-year base patterns or medium-term consolidation patterns and have been outperforming the broad markets for quite a few weeks now.

This is particularly bullish for the S&P/TSX Composite where these stocks comprise more than 30% of the capitalization of the index, i.e., the S&P/TSX has been outperforming the S&P 500 for most of the past three months and the expectation is that trend is likely to continue for the remainder of 2024 and likely into 2025.

Federal Reserve: The Time Has Come!

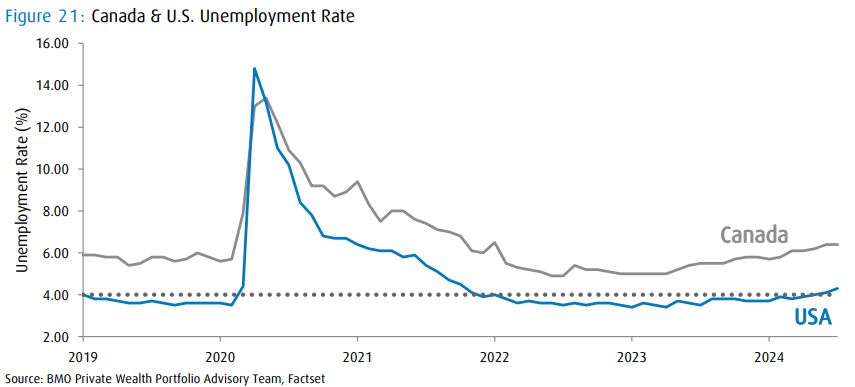

After weeks of speculation, Fed Chair Powell finally confirmed that the time has come for the policy to be adjusted. Progress on the inflation front is certainly providing the flexibility for the Fed to ease but it is the concern over the softening of the labour market that seems to now dictate timing and magnitude of the first cut. In particular, the unemployment rate rising above 4% is seen as a yellow flag for the economy.

However, before fearing a recession yet, it is important to note that unlike previous economic downturns, the rise in the unemployment rate is not led by a significant increase in layoffs. It is instead a combination of slower hiring and an increase in the participation rate (pool of individuals available to work) that pushed the unemployment rate to its highest level since January 2022. We certainly do not want to dismiss the recession risk, a risk worth monitoring closely, but we are encouraged by the Fed’s willingness to ease policy to help achieve an economic soft landing over time. We are also encouraged by the mild signal from our Nesbitt Burns Recession Risk Model that shows less than 50% risk over the next 12 months.

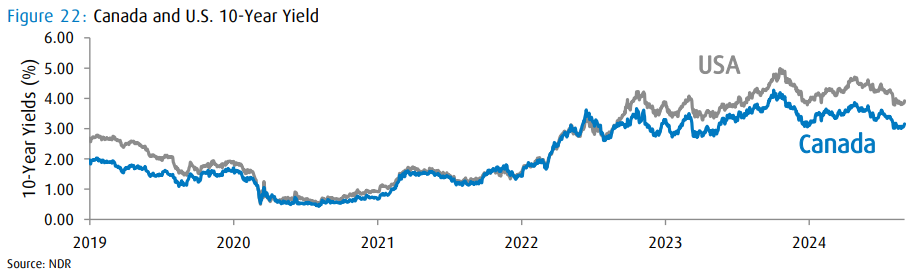

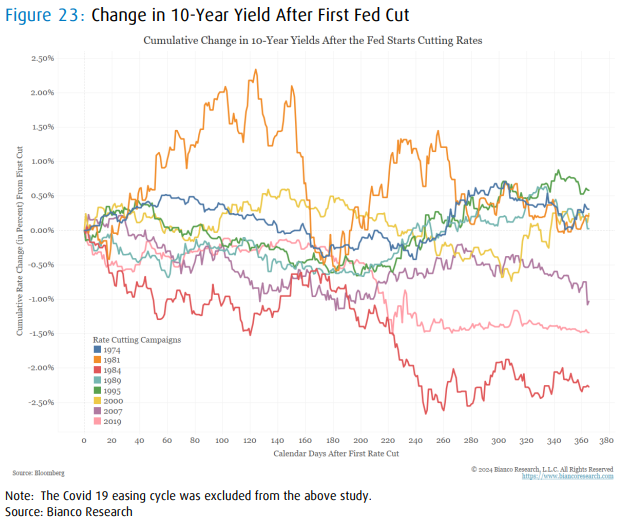

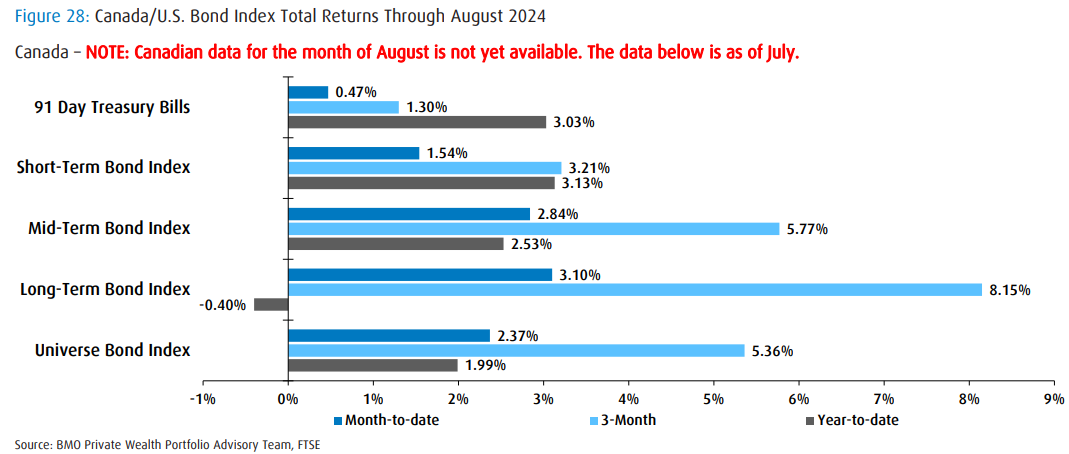

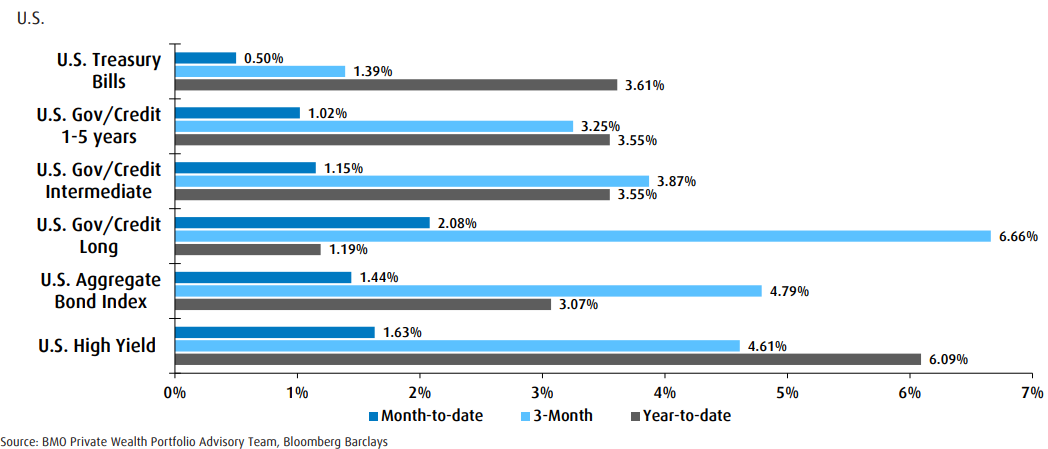

For bond markets, expectation of lower Fed policy rates has been behind the lower U.S. Treasury yields and re-steepening of the yield curve; short-term rates declined faster than long-term rates so far in 2024. Most economists – including BMO – now expect three consecutive 25 basis points (bps) cuts before year-end which are fully priced in the market. In fact, the market even sees the possibility of one 50 bps cut should economic conditions deteriorate further. Considering that interest rates declined further in August and barring any negative economic surprises (e.g., CPI, labour), we believe the U.S. Treasury yield market is well priced and offers limited capital gains potential, leaving bonds to earn their yields for the second half of 2024. Nothing wrong with this, but investors will objectively need to adjust lower performance expectation for the remainder of the year compared to the first eight months. The experience from previous easing cycles also suggests capital gains from lower mid- to long-term rates may be more muted in the near term. Figure 23 below from Bianco Research shows the cumulative change in 10-year yield in the 365 days that followed the first Fed rate cut and with small exceptions, the 10-year yield tend to remain relatively rangebound.

There are two notable experiences that would suggest otherwise: 1984 and 2019. However, it is important to note that in 1984, the Fed did not broadcast rate cuts as it is doing today. As for 2019, after starting its easing cycle in the summer, Covid 19 forced the Fed to significantly alter policy in March 2020.

General Disclosure

The information and opinions in this report were prepared by BMO Private Wealth Portfolio Advisory Team (“BMO Private Wealth”). This publication is protected by copyright laws. Views or opinions expressed herein may differ from the views expressed by BMO Capital Markets’ Research Department. No part of this publication or its contents may be copied, downloaded, stored in a retrieval system, further transmitted, or otherwise reproduced, stored, disseminated, transferred or used, in any form or by any means by any third parties, except with the prior written permission of BMO Private Wealth. Any further disclosure or use, distribution, dissemination or copying of this publication, message or any attachment is strictly prohibited. If you have received this report in error, please notify the sender immediately and delete or destroy this report without reading, copying or forwarding. The opinions, estimates and projections contained in this report are those of BMO Private Wealth as of the date of this report and are subject to change without notice. BMO Private Wealth endeavours to ensure that the contents have been compiled or derived from sources that we believe are reliable and contain information and opinions that are accurate and complete. However, BMO Private Wealth makes no representation or warranty, express or implied, in respect thereof, takes no responsibility for any errors and omissions contained herein and accepts no liability whatsoever for any loss arising from any use of, or reliance on, this report or its contents. Information may be available to BMO Private Wealth or its affiliates that is not reflected in this report. This report is not to be construed as an offer to sell or solicitation of an offer to buy or sell any security. BMO Private Wealth or its affiliates will buy from or sell to customers the securities of issuers mentioned in this report on a principal basis. BMO Private Wealth, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO Private Wealth or its affiliates may act as financial advisor and/or underwriter for the issuers mention we herein and may receive remuneration for same. Bank of Montreal or its affiliates (“BMO”) has lending arrangements with, or provides other remunerated services to, many issuers covered by BMO Private Wealth’ Portfolio Advisory Team. A significant lending relationship may exist between BMO and certain of the issuers mentioned herein. BMO Private Wealth is a wholly owned subsidiary of Bank of Montreal. Dissemination of Reports: BMO Private Wealth Portfolio Advisory Team’s reports are made widely available at the same time to all BMO Private Wealth investment advisors. Additional Matters TO U.S. RESIDENTS: Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Capital Markets Corp. (“BMO CM”) and/or BMO Private Wealth Securities Ltd. (“BMO NBSL”). TO U.K. RESIDENTS: The contents hereof are intended solely for the use of, and may only be issued or passed onto, persons described in part VI of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001.

BMO Wealth Management is the brand name for a business group consisting of Bank of Montreal and certain of its affiliates, including BMO Private Wealth, in providing wealth management products and services. BMO Private Wealth is a Member-Canadian Investor Protection Fund and a Member of the Investment Industry Regulatory Organization of Canada