Rates Scenario | An outlook on key interest and foreign exchange rates

BMO Private Wealth - Oct 11, 2024

We’ve made no major changes to our Federal Reserve and Bank of Canada calls since our last Rates Scenario (September 12), despite the Fed’s surprise 50-bp rate cut last month.

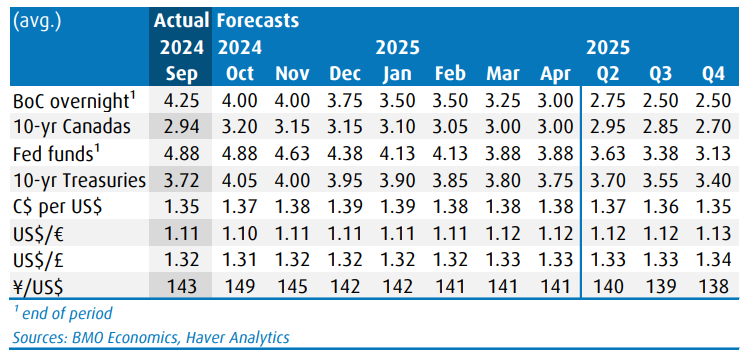

Forecast Summary

Canada-U.S. Rates Outlook

Staying the Course

• We’ve made no major changes to our Federal Reserve and Bank of Canada calls since our last Rates Scenario (September 12), despite the Fed’s surprise 50-bp rate cut last month. We look for both central banks to continue reducing policy rates until they are in the neutral realm. This is a 2.75%-to-3.00% target range for the Fed funds rate, the midpoint of which is also the FOMC’s new (higher) median projection for the longer-run level. We expect to hit this by March 2026, as before, but the anticipated downshift to acting only quarterly now starts after March 2025 instead of June. For the Bank of Canada, this is a 2.50% overnight rate target, which is a bit below the midpoint of the Bank’s 2.25%-to-3.25% range for the neutral rate. As before, we expect to hit this by July 2025. Finally, despite selling off recently, we reckon bond yields will still drift down to the levels we previously envisioned against the background of both central banks cutting rates and core inflation falling further.

• Federal Reserve: The FOMC surprised with a 50 bp rate cut on September 18. The previous times when the Fed commenced a rate cut campaign with 50 bps were 2007, during the Global Financial Crisis, and 2001, during the ‘tech wreck’. With no financial crisis currently, this begged the question: ‘What does the Fed know that we don’t know?’ It turns out this was more about what the Fed didn’t know. Powell said if the Fed had the July employment report in hand for the July 31 FOMC confab (it was released two days later), “we might have well” cut rates at the time. In some respect, September’s move was a catch-up for not starting the meeting before. Powell called it a "recalibration" designed to push “policy down over time to a more neutral level” and, in a manner “to make sure that we don’t fall behind”.

• Even before the latest stronger-than-expected employment and CPI reports for September, the Fed was signalling that subsequent rate cuts would be the 25 bp variety. At a September 30 event, Powell said: “This is not a committee that feels like it is in a hurry to cut rates quickly.” And, amid these reports, the market has flipped from considering the odds of a follow-up 50-bp action (which topped 55% late last month) to a pause (currently 15%- to-20%) at next month's meeting. We highly doubt the Fed will pause in the wake of these reports.

• The rate-cut criterion of the Fed gaining “greater confidence that inflation is moving sustainably toward 2 percent” has been satisfied, and one round of unanticipated stickiness isn’t going to undermine this. On the other mandate, in the post-FOMC presser, Powell said we’re “pretty close to what I would call maximum employment” and “we don’t think we need to see further loosening in labor market conditions to get inflation down to 2 percent”. This assertion was made with August data in hand, and one month of unexpected strength isn’t going to alter this assessment either. But at the prevailing level of policy restrictiveness, such loosening is what would likely unfold. Recall Powell’s Jackson Hole declaration: “We do not seek or welcome further cooling in labor market conditions.”

• Measuring policy restrictiveness by the real fed funds rate (nominal less core PCE inflation), the 2.7% that prevailed in August was well above the FOMC’s current 0.4%-to-1.8% range for the neutral level with its 0.9% median. The Fed’s big 50 bp move roughly chopped in half the distance to the top of the range, pending what happens to core PCE inflation in September and October. The Fed has more easing wood to chop if it wants to avoid causing unnecessary labour market weakening. And more cuts are being signaled. The Summary of Economic Projections and its ‘dot plot’ showed the median FOMC projection with a further 50 bps of cuts for this year (in line with our thinking) and 100 bps next year (we’re at 125 bps).

• Bank of Canada: Even before the Fed’s rate cut surprise, the market had been musing about the potential for a 50 bp BoC rate cut, after a third consecutive 25 bp reduction on September 4. The data contributed to the market buzz, with the unemployment rate having risen another notch to 6.6% for August (up 0.9 ppts from this year's low) and total CPI inflation falling 0.5 ppts to hit the 2.0% y/y target (and the slowest pace in 3½ years). In a mid-September interview (before the Fed announcement), Governor Macklem said: “As you get closer to the (inflation) target, your risk management calculus changes… You become more concerned about the downside risks. And the labour market is pointing to some downside risks.” He added that “it could be appropriate to move faster (on) interest rates” if economic growth came up short. Macklem asserted: “We don’t want to see more slack” in the economy.

• The Fed’s rate cut only pumped this speculation further. But, as U.S. market odds of a follow-up 50-pointer have since faded, market conviction in a 50-bp BoC rate cut has buckled as well. Causing more buckling, September’s Labour Force Survey showed a tenth dip in the jobless rate to 6.5% with employment up a strong 47k (with full time jobs up an even stronger 112k). The tone of the Bank’s Business Outlook Survey for Q3 was still negative but trending less so. Unless the September CPI report screams excessive disinflation, the policy scale appears to be tipping much more to the 25 bp side (than to the 50 bp side). In turn, we look for the run of consecutive quarter point rate cuts to continue through mid-2025. But as real GDP per capita continues to contract, the output gap continues to widen, and the unemployment rate continues to climb (to at least 7%), the risk of the Bank easing more aggressively (by 50 bp increments) or to a lower endpoint (below 2.50%) remains substantial.

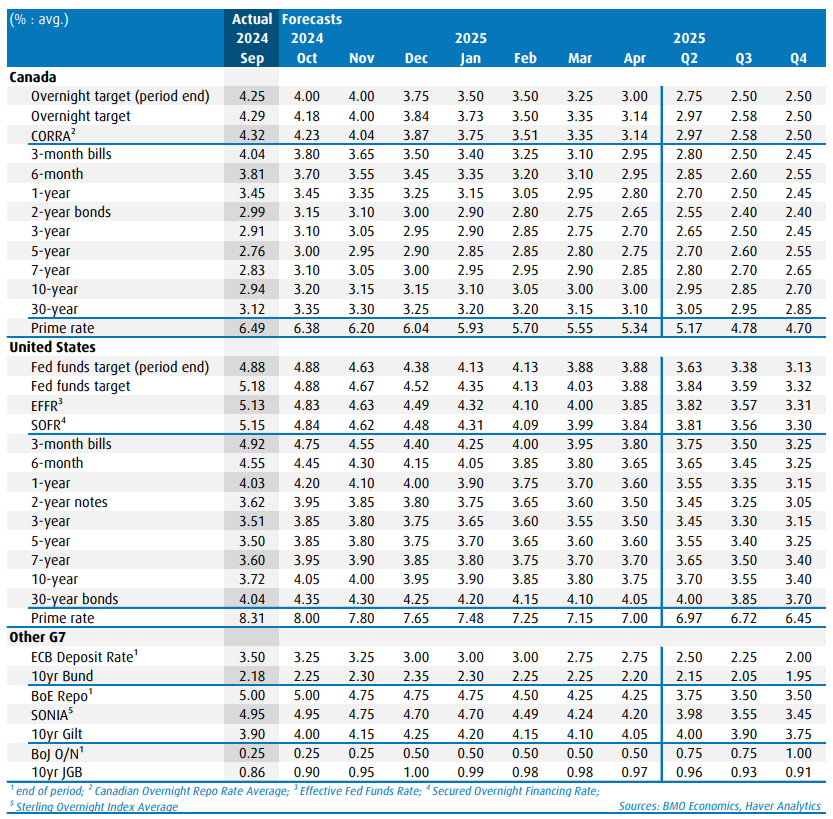

• Bond yields: Ten-year Treasury yields averaged 3.72% in September, below the 4% mark for the second consecutive month after a one-year run above it. October began similarly (it closed at 3.74% on the 1st) but the parade of stronger-than-expected economic data, particularly the employment report, helped push the daily mark back above 4%. October is on track to average around 4.05% (should the latest close hold), with the market paring back its Fed easing prospects. However, once it’s clear rate cuts are continuing (come November 7), we look for yields to drift back below 4% and for the downtrend to last as the Fed eases further and core PCE inflation ebbs. Yields should average lows under 3.40% toward the tail end of the Fed’s rate cut campaign. However, once the Fed is finished easing, we expect yields to eventually embark on a gradual trend back to the 4% mark. The uptrend reflects the combination of persistently large budget deficits (regardless of November’s election outcome) and lingering inflation risks owing to the economic duo of deglobalization and decarbonization.

• Meanwhile, 2-year Treasury yields averaged 3.62% in September, ending a 26-month run of an inverted yield curve. This month is on track to average around 3.95%, maintaining the curve reversion. As with 10s, we look for a resumed downtrend in 2s to be unfolding when the Fed next cuts rates. At the trough in policy rates, we look for 10s-2s to be averaging in the 55-to-65 bp range. • Ten-year Government of Canada yields averaged 2.94% in September, slipping below the 3% mark for the first time in 22 months and resulting in Canada-U.S. yield spreads of -78 bps. The latter has been grinding less negative since June's record -92 bps. Canada 10-year yields are on track to average above 3.20% this month, selling off slightly less than Treasuries (not surprising) and causing Canada-U.S. spreads to move back into the low -80 bp range. However, next month, once yields have resumed declining on both sides of the border, we see Canada's again lagging and spreads resuming their less-negative grind, heading to the -70 bp average mark. Meanwhile, 2-year Canada's averaged 2.99% last month, with the 10s-2s spreads at -5 bps, the smallest degree of curve inversion since it started in July 2022. After the Bank’s expected (25 bp) action this month, we look for the curve's slope to finally flip positive on a sustained basis.

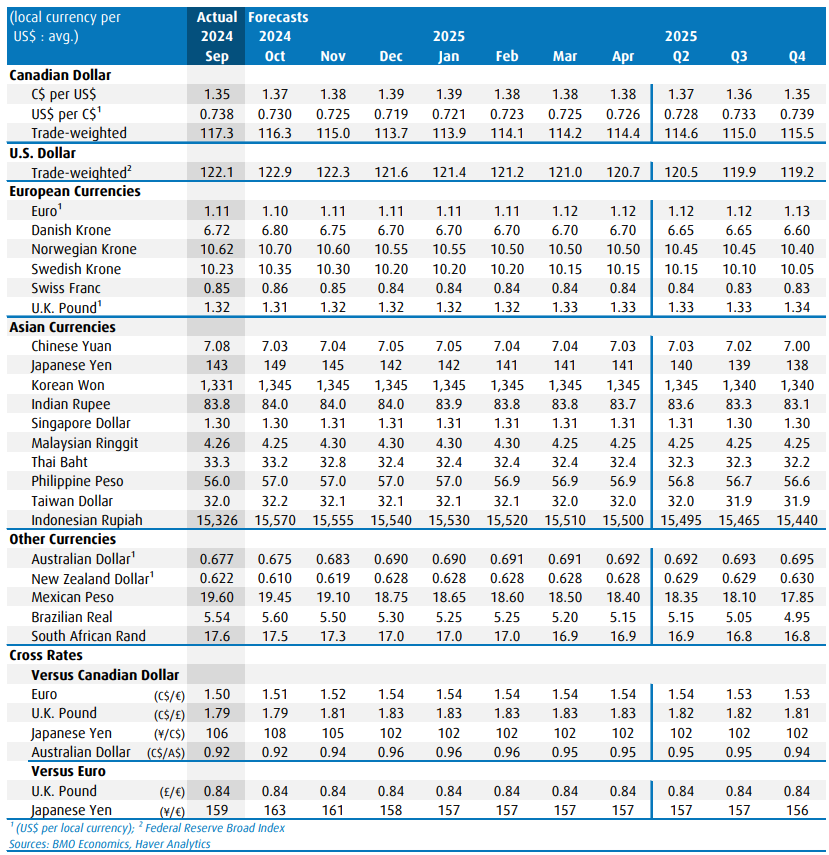

• U.S dollar: The Fed’s trade-weighted dollar index averaged 0.6% weaker in September after falling in both July and August (for a cumulative 1.5%), as the market increasingly braced for a Fed rate cut and then got a larger-than expected one. Before the three-month slide, in June, the greenback was being pushed stronger as other central banks were jumping on the easing bandwagon and the Fed was not. Indeed, June boasted the strongest level since the autumn of 2022 when the currency was backing off from record highs (when fears over Fed policy rates remaining ‘higher for longer’ were running rampant). This emphasizes how dominant Fed policy prospects can be for the U.S. dollar.

• However, this month, the greenback is on track to gain back about half the above-mentioned cumulative decline, reflecting the market’s shift in Fed policy speculation from 25 vs. 50 to 25 vs. pause, along with escalating geopolitical risks (with Middle East tensions particularly on the rise). As rate cuts continue (and presuming geopolitical risks calm), we see the big dollar down about 1¼% by the end of this year (compared to October’s tracking) and a further roughly 2¼% next year.

• Canadian dollar: The loonie averaged C$1.355 (US$0.738) last month, appreciating 0.8% and doubling up on August’s advance, aided by the anticipation and realization of a Fed policy rate cut. Before, the currency had tested its weakest readings since the immediate onset of the pandemic during June and July (a bit above C$1.37 or below US$0.73), owing to a pair of Bank of Canada rate cuts that pushed Canada-U.S. overnight spreads more negative by about 50 bps (to around -80 bps for CORRA-EFFR). The BoC's third consecutive cut on September 4 pushed spreads to around -105 bps, the most negative in more than 17 years, but the loonie took it in stride with a Fed rate cut looming (which in one fell swoop pushed overnight spreads back to the -50/55 bp range).

• However, this month, the loonie is on track to give back almost all of September’s gain and then some, reflecting the market’s shift in Fed policy speculation and escalating geopolitical risks. Then there’s the more perennial problem of Canada’s much weaker (than U.S.) economic and productivity performance and associated risk of more aggressive (than Fed) BoC actions. Indeed, we reckon this factor alone will, on net, sway the loonie (weaker) until it is clear Canada’s dimming economic prospects are brightening. We see the Canadian dollar averaging $1.390 (US $0.719) by year-end, before finally benefiting from Fed-policy-driven, broad-based, greenback weakness. By the end of next year, we see the loonie gaining 3%.

Overseas

• Just a month or so ago, markets were not paying too much attention to the October ECB meeting. Remember: the official message at the September meeting was that it would be too soon to move since there would not be a lot of new information between meetings to justify it. However, it is no longer as clear-cut; in fact, there is a strong case for the ECB to lower rates again on October 17. The concerning news for Germany, for example, continues to stack up, such as the latest readings for the PMIs and the Ifo survey. Then there is Volkswagen, which is Germany’s largest private sector employer. For the first time in 87 years, the automaker is considering closing a number of plants across the country, and axe jobs. (Moody’s took notice and downgraded its outlook on the firm.) Intel is also putting its plan to build a semiconductor factory in Germany on hold for two years, dashing the Euro Area’s plans to produce 20% of the world’s semiconductor supply. The German government, as well as the Five Wisemen, expects the economy to shrink for the second year in a row. Instead of 0.2% growth, a 0.3% contraction is now penciled in for 2024. In the words of Economy Minister Habeck, fingers are pointing to “failures of recent decades”. Meantime, on the inflation front, over half of the Euro Area has below-target inflation as of September. The broader Euro CPI reading is at 1.8%, down from 2.2% in August. This is the first time it has been below target since June 2021 and the lowest since April 2021. Compare that to the high of 10.6% back in October 2022 and discuss among yourselves. Core CPI also cooled a bit, from 2.8% in August to 2.7%, and services CPI to 4.0% (still high) from 4.1% in August. Even Executive Board member Isabel Schnabel has toned down her hawkish remarks. In any event, although it is not a done deal for the central bank, we now expect the ECB to succumb to the mounting pressure for earlier cuts and lower the deposit rate in both October and December, by 25 bps each time.

• Rate cut expectations are rising in the U.K. as well... not the cut itself, but the size. Recall that the BoE has been far more reluctant to ease policy (stronger growth; stubborn inflation; and a really, really, divided MPC), and has only made one 25 bp reduction (back in August) compared to two by the ECB, three by the BoC and one large one by the Fed. But that may change. BoE Governor Andrew Bailey recently sent the GBP spiralling lower after he told the media that if inflation comes down faster than expected, the BoE could be "a bit more aggressive" on the rate-cutting front. That sparked expectations of a 50 bp rate cut, which seems rather extreme given that there is still a number of policymakers who remain hawkish, even when voting for no change in policy at the last meeting. And, the data so far hardly push for such an aggressive move. Chief Economist Huw Pill calmed nerves a couple of days later when he warned that there is a risk of cutting rates "too far, and too fast." This is not the first time that both central bankers are at odds. We continue to stand by our call for a 25 bp rate cut on November 7, while reserving the right to tweak that call depending on Chancellor Reeves' budget, to be tabled on October 30.

• Meantime, the BoJ has a decent case to plead for patience on the tightening front, as the economic data are pointing to a rather sluggish Q3. For example, industrial production took a large 3.3% step back in August, and though some blame can be placed on the auto sector's regulatory scandal (Toyota admitted it faked safety tests on some of its models), it is not a good look for Q3 growth. At least retail sales surprised to the upside, rising 0.8% in August alone, or 2.8% above a year ago. And, Japan's job market tightened up in August. The jobless rate slipped from 2.7% to a lower-than-expected 2.5%, landing it back around the Q1 average. There is also political pressure, with the new PM and one of his close advisors telling Governor Ueda that tightening now would be bad for the economy. Nonetheless, with inflation still running above target and rates still very low at 0.25%, there is a case to be made that the BoJ can continue to move slowly towards normalization without jeopardizing growth. The recent selloff in the JPY doesn't help the inflation outlook either, nor does the run-up in energy prices. And not tightening again in December could be viewed as succumbing to political pressure. The Bank is in a tough spot. We still expect the Bank to tighten the screws a bit more in December.

• And how about that RBA? Up until the September meeting, policymakers only had two options on the table: hike or hold, due to its ongoing concerns about persistent inflation. The September statement was still hawkish, as it did not see inflation returning to target until 2026. But recall that Governor Bullock seemed to play down the possibility of a rate hike during the press conference when she revealed that there was a discussion around their messaging, and that the Board "didn't explicitly consider" a rate hike as not enough had changed since the prior meeting. Well, according to the Minutes, the 'cut' option also came up for consideration, given a series of ifs... if the economy and the labour market became significantly weaker; or if households saved more than the central bank assumed, due to a softer job market or more uncertainty. In other words, all possible outcomes were discussed. At the end, the Board decided to remain "vigilant" to the upside risks of inflation and will continue to rely on the data to determine what to do next. It did acknowledge rate cuts made by other central banks but that in Australia, "the labour market was stronger and monetary policy less restrictive". Of course, this was before the RBNZ's 50 bp cut on October 9. Meantime, we are still fairly comfortable with the view that a rate cut will eventually come in December.

Foreign Exchange Forecast

Interest Rate Forecasts

BMO Private Wealth is a brand name for a business group consisting of Bank of Montreal and certain of its affiliates in providing private wealth management products and services. Not all products and services are offered by all legal entities within BMO Private Wealth. Banking services are offered through Bank of Montreal. Investment management, wealth planning, tax planning, philanthropy planning services are offered through BMO Nesbitt Burns Inc. and BMO Private Investment Counsel Inc. If you are already a client of BMO Nesbitt Burns Inc., please contact your Investment Advisor for more information. Estate, trust, and custodial services are offered through BMO Trust Company. BMO Private Wealth legal entities do not offer tax advice. BMO Trust Company and BMO Bank of Montreal are Members of CDIC.

® Registered trademark of Bank of Montreal, used under license.